Moving Into the Future: Technological Trends in Banking

As with almost every industry, banking benefits from the latest technologies. Many financial institutions have already implemented mobile banking apps and AI-controlled chatbots. However, the future of banking lies with a series of emerging technologies designed to increase efficiency and customer experience. Here’s a look at some of the technological trends that may change the shape of banking.

Blockchain Technology

Blockchain may bring one of the largest overhauls to the modern banking system. While blockchain technology is mostly associated with Bitcoin, the potential uses of the technology extend far beyond cryptocurrencies. Close to 75 percent of banks are in the early stages of adopting blockchain technology. An online ledger that is essentially managed by a network of computers, using blockchain means that every computer on a blockchain network stores a copy of that ledger, creating a transparent record. Previous transactions cannot be altered without altering every copy of the ledger, which also increases the security of blockchain compared to other data management systems. Most ledgers are managed by a peer-to-peer (P2P) network. However, banks may develop private ledgers for internal use. While this eliminates the transparency of an open ledger, it still provides major security benefits. Adopting blockchain gives banks a secure solution for instant money transfers as well, which benefits both consumers and banks. Consumers benefit from lower fees and shorter waiting periods, while banks benefit from increased efficiency, fewer errors, increased security, and lower overhead.

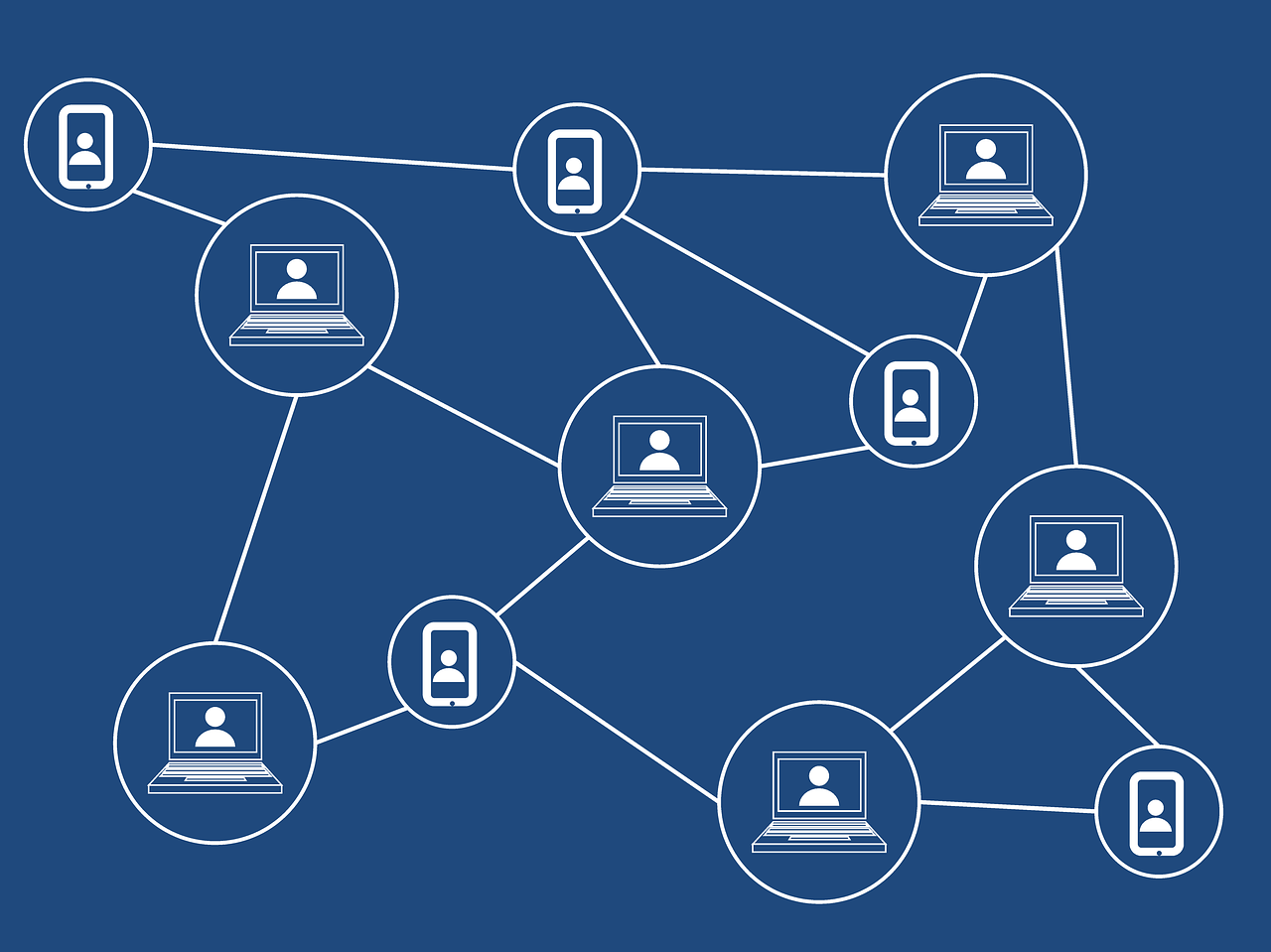

Peer-to-Peer Payments

About 40 percent of financial institutions have proposed investment in peer-to-peer (P2P) payment systems in 2020. While PayPal is the most recognizable consumer P2P payment app, over 80 percent of the largest banks use Zelle as a P2P payment provider. A P2P payment system is simply a way for customers to complete electronic money transfers to other accounts. Integrating P2P payment allows banks to give customers flexible solutions, as well as remain competitive in an increasingly online world. P2P payments, meanwhile, can also benefit from blockchain technology. In an open banking system, a distributed ledger can ensure the security of each P2P transaction. All transactions are permanently added to the ledger, reducing the risk of fraud and providing greater transparency.

Digital Account Opening

Almost a third of banks plan on implementing new or replacement software to handle digital account opening (DAO). DAO allows customers to open accounts without physically visiting a bank – a boon not only to consumers in an increasingly digital age, but also to more and more remote workers who may be moving abroad or traveling. Due to the online environment, DAO comes with additional security and regulatory concerns, however. Banks need to cautiously verify the identity of a customer when opening an account. They must also evaluate the risk of each applicant and obtain funds electronically in real time. These potential concerns have slowed the adoption of DAO solutions, however, many banks are now investing in DAO software to avoid missing out on this growing segment of the banking market. With younger generations of adults preferring online interactions for goods and services, a recent study found that 75 percent of millennials prefer opening a bank account online. As dozens of new online banks open each month to cater to millennials, traditional financial institutions are implementing DAO options to keep up with the demand.

Machine Learning

Artificial intelligence (AI) is currently used in a variety of implementations from chatbots to personalization features in web-based services. However, the use of these technologies is dwindling, as the real future of AI is the ability to analyze big data through machine learning. Allowing powerful computers to analyze large volumes of data provides many practical uses in the banking industry. Large financial institutions may employ machine learning to automate processes or devise new strategies, while machine learning may also change the future of fraud detection. AI technology can analyze and detect suspicious activity more efficiently compared to existing systems, and reducing fraud, along with the time spent dealing with fraud prevention, offers significant value in the banking industry. In addition to internal processes, AI and machine learning may improve the customer experience as well, with chatbots and personalization just the beginning. For banks, implementing this technology now makes it easier to remain on the cutting edge of AI as it develops into the future.

Cloud Computing

Blockchain technology and machine learning systems require substantial information technology resources. Instead of increasing their on-site IT infrastructures, many financial institutions are moving to the cloud. Close to 50 percent of banks already use cloud computing, and many intend to enhance their existing solutions. Adopting cloud technology offers many advantages in the banking industry, including improved cybersecurity, reduced IT infrastructure costs, faster technology implementation, and access to more powerful technologies. Using cloud-based servers to manage data and applications is becoming more secure compared to on-site systems as well. Many cyberattacks are directed at poorly managed IT networks, with smaller banks being the biggest targets, as they tend to lack the sophisticated security features used at major financial institutions. Transitioning to cloud-based services reduces IT costs, meanwhile, by saving banks money on hardware, staffing, and future technologies. Implementing updates and new tech is often faster and cheaper when dealing with cloud computing, which provides direct access to the latest developments.

Application Programming Interfaces (APIs)

Application programming interfaces (APIs) are not new. The IT industry has used APIs for over two decades to simplify software implementation for third parties. However, the banking industry is just now starting to invest heavily in the creation of their own APIs. Working as an interface that establishes communication between two sets of software, organizations typically use APIs to give third-party developers access to assets such as data or other specific services. Google, for example, offers APIs for most of its web-based services, allowing independent developers to implement Google Maps or Gmail in their applications. In the banking industry, an API provides a simpler interface for integration with vendor software or custom applications. Banks can also make their APIs available to organizations to develop tools that fit their industries, providing a secure communication between the bank’s data or resources and third-party software, and giving clients greater freedom to develop custom solutions.

Some technologies receive a lot of attention without delivering long-term results. While large financial institutions are investing billions in these trends, some smaller banks may choose to hold off until they can review concrete statistics. But with major banks investing heavily in AI, cloud computing, and APIs, many financial institutions around the world are already rolling out many of these technologies, and they will continue to develop in the years to come.